Monthly Market Recap – December 2023

The Highlights (and Lowlights) of 2023…

Inflation, and the Federal Reserve’s response to it, continued to get the spotlight throughout the year. After beginning an aggressive war on inflation in March of 2022, inflation stood at about 6.5% to start 2023, well above the Federal Reserve’s target of 2%. High inflation and high interest rates raised concerns of rising unemployment and a looming recession to start the year.

While the Federal Reserve continued to battle recession throughout the year, a few other things of note happened as well: a political fight over the debt ceiling, labor strikes, bank failures, unrest in the Middle East, and a near government shutdown that ultimately led to Speaker of the House, Mike McCarthy, being ousted from his role.

As the Federal Reserve continued to raise interest rates throughout the first half of the year, evidence of their efforts began to show as inflation started to fall, but it also contributed to the bank failures as well as the unfortunate effect of cooling the housing market. Rising interest rates also carried over to mortgage rates, which vaulted higher to a multi-decade high of about 8.0% in October. Fortunately, mortgage rates have fallen by more than a full point over the last few months of the year, settling at about 6.61% at the end of December.

Surprising to most is that the economy and the labor markets remained relatively strong throughout the year. Gross domestic product was positive in each quarter, especially the 3rd quarter, measuring a robust 4.9%. Job openings decreased throughout the year as did the number of new jobs, but the unemployment rate remained near historical lows throughout much of the year, ranging between 3.5%-3.8%.

As the year came to a close and we were busy wrapping presents, the Federal Reserve wrapped up their last meeting of the year in December. The markets gave investors the gift of a Santa Claus market rally in response to the Federal Reserve’s indication that no more rate hikes were anticipated, as well as pivoting to a more dovish stance by projecting three rate cuts in 2024.

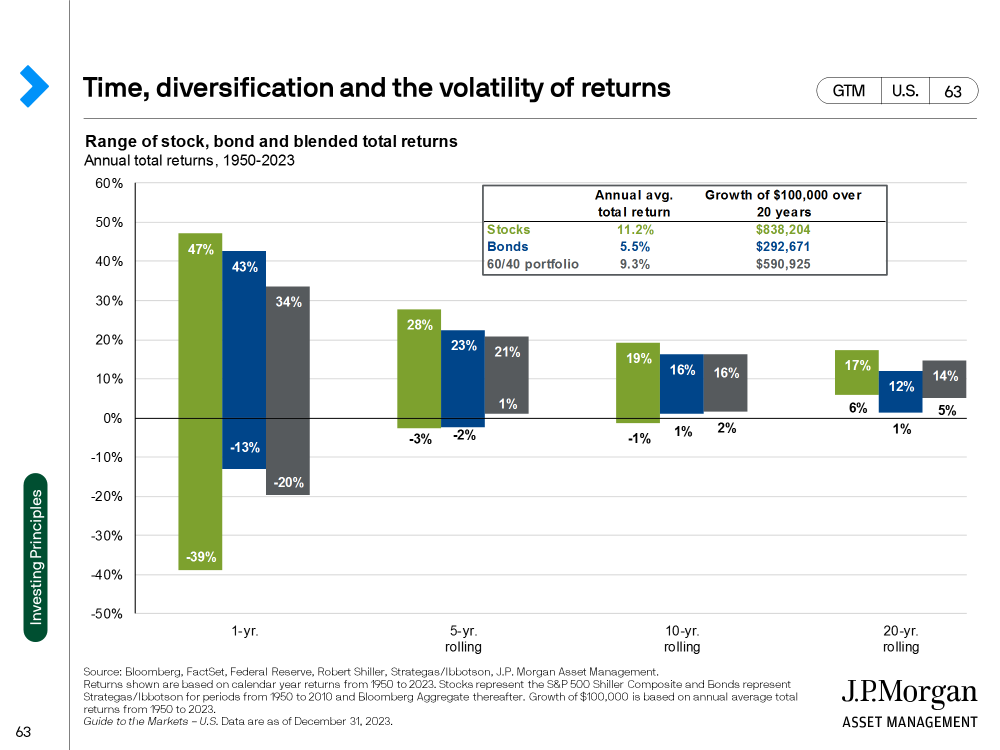

Did you know? Since 1950, the annual average total return for the S&P 500 index is 11.2%. In 2023 we experienced some abnormally positive returns. In 2022 we experienced some abnormally negative returns. This is why we continue to believe in diversified portfolios aligned with clients’ risk tolerance, time horizon and financial goals.

Stocks rallied into the end of the year. The Dow Jones Industrial Average rose 4.9%, the S&P 500 advanced 4.5%, and the NASDAQ jumped 5.6%. Small-caps had a particularly standout month, as the Russell 2000 surged 12.2% in December. For the year, the Dow logged a 16.2% gain, the S&P 500 added 26.3%, and the NASDAQ blazed higher by 44.6%.

*10

*1

All eleven sectors posted a positive December. Real Estate led the way with an 8.8% increase, followed by a 7.1% advance in Industrials and 6.1% in Consumer Discretionary. Technology, Communication Services, and Consumer Discretionary were the best-performing sectors in 2023, while three sectors recorded a down year: Energy, Consumer Staples, and Utilities.

*2

The Economic Data Rundown

US Treasury Yields

Treasury yields fell further in December as investors continued to pile into equities. Longer-term instruments saw larger declines, as yields on the 20-year and 30-year fell by 52 and 51 basis points, respectively. The 5-year and 10-year both tumbled below 4%, resulting in meaningful price appreciation across much of the fixed income asset class.

Consumers and Inflation

The US inflation rate continued its Year-over-Year (YoY) slide, falling to 3.14% in November, which is the lowest print in 5 months. Core Inflation slowed to 4.01%, its lowest YoY level since September 2021. The monthly US Consumer Price Index inched 0.1% higher, and monthly US Personal Spending grew a quarter of a percent in the same month. With continued progress on reigning in inflation, the Federal Reserve held its key Fed Funds Rate at 5.50% at its December 13th, 2023 meeting, marking the Fed’s third consecutive meeting in which rates were left unchanged.

Production and Sales

The US ISM Manufacturing PMI remained unchanged at 46.7 in November and in contraction territory for the 13th consecutive month. November US Retail and Food Services Sales rose 0.28% Month-over-Month (MoM) after contracting for the first month in the last eight, while the YoY US Producer Price Index fell for the second straight month to 0.86%.

Housing

US New Single-Family Home Sales plummeted 12.2% MoM in November, while US Existing Home Sales inched 0.8% higher MoM. However, the Median Sales Price of Existing Homes fell for the fifth straight month to $387,600 in November. The median price of existing homes is 6.33% below its all-time high. Mortgage rates continued their cooldown into December; the 15-year Mortgage Rate ended the year at 5.93%, below 6% for the first time since May. The 30-year closed out 2023 at 6.61%, falling below 7% for the first time since mid-August.

Commodities

The price of Gold ended the year at $2,062.28 per ounce, representing a monthly increase of 1.32%. Crude oil prices were largely unchanged MoM despite having encountered some price volatility within December. As of Christmas Day, the price of WTI per barrel was $75.84 while Brent was $80.23. December brought drivers the lowest average price of gas in 2023, which was $3.18 per gallon on December 18th. The last time the average price of gas was that low was June of 2021.

*3, 4, 5, 6, 7, 8, 9

As always, don’t hesitate to contact us if you have any questions about what impact, if any, this may have on your financial plan.

For more great insights, highlights, and financial education,

follow MDL Wealth Management on:

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk.

The economic forecasts set forth in this material may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

3Department of the Treasury

4Bank of America Merrill Lynch

5Federal Reserve

6University of Michigan

7Bureau of Labor Statistics

8Institute for Supply Management

9Census Bureau