Monthly Market Recap – September 2023

The Summer Slide

Stocks continued to decline in September as the Dow Jones Industrial Average fell 3.4%, the S&P 500 slipped 4.8%, and the NASDAQ ended 5.8% lower. Around the world, Emerging Markets were down 2.6%, and EAFE sank 3.4%. September’s declines dragged equities into the red for Q3. The Dow posted a 2.1% decline in Q3, the S&P 500 ended the quarter down 3.3%, and the NASDAQ 3.9% finished lower. Fixed Income also moved lower as interest rates rose. The Bloomberg US Aggregate fell 2.54% in the month.

*10

*1

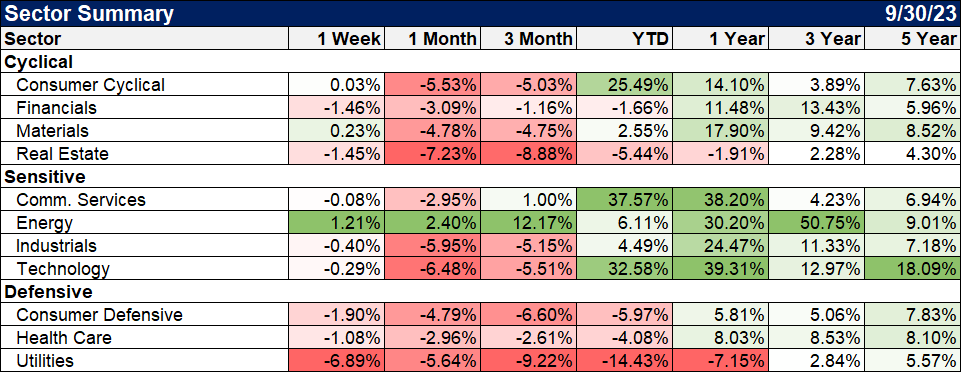

For the second straight month, Energy was the only US stock sector to post a positive return. Real Estate was the top laggard in September, tumbling 7.2%.

*2

The Economic Data Rundown:

US Treasury Yields

Yields on longer-term treasuries increased in September as T-Bills ended the month broadly unchanged. The 20-year and 30-year bonds each rose by 53 basis points. The 10-year’s 50 basis point increase helped reduce the inverted 10-2 treasury yield spread to -0.44%. The Federal Reserve kept the benchmark Target Federal Funds Rate unchanged at 5.50% during its recent September 20th meeting but remained hawkish.

Employment

August’s unemployment rate rose to 3.8%, three-tenths higher than July’s figure of 3.5%. However, the labor force participation rate grew by two-tenths to 62.8%. In August, 187,000 jobs were added, surpassing nonfarm payrolls expectations of 170,000. However, the latest Job Opening and Labor Turnover Survey, or JOLTS report, is still reflecting a resilient labor market. The most recent report reflected that there were 9.6 million jobs open at the end of August, an increase from the 8.92 million job openings in July.

Consumers and Inflation

Year-over-year (YoY) inflation rose for a second straight month, from 3.18% in July to 3.67% in August. Conversely, Core Inflation fell to 4.35% in August, marking the fifth consecutive monthly decline. The US Consumer Price Index logged a monthly increase of 0.63% in August, its most prominent in the last 14 months. US Personal Spending was up 0.45% month-over-month (MoM).

Production and Sales

The US ISM Manufacturing PMI increased by 1.4 points in September to 49.0. This is the third consecutive monthly increase as the key manufacturing index approaches 50, the dividing line between expansion and contraction. US Retail and Food Services Sales grew by 0.56% MoM in August, and the YoY US Producer Price Index jumped to 1.6%.

Housing

US New Single-Family Home Sales contracted 8.7% in August, following a July in which new home sales grew by 8.0%. US Existing Home Sales sank for the third consecutive month, down 0.7%, and 17th out of the last 19. The Median Sales Price of Existing Homes inched 0.3% higher to $407,100, staying above $400,000 for the third straight month. Mortgage rates pushed higher in September: 15-year and 30-year Mortgage Rates ended the month at 6.72% and 7.31%, respectively.

Commodities

The price of Gold fell 3.7% in September, from $1,942.30 down to $1,870.50. WTI oil per barrel briefly reached $90 in September, ending the month at $89.68, an increase of 7.3%. Brent rose 7.7% in September to $94.01 per barrel. As a result, the average price of regular gas also eclipsed $4.00 per gallon in mid-September, settling at $3.96 as of September 25th.

*3, 4, 5, 6, 7, 8, 9

Key Takeaways:

1) The Federal Reserve began raising interest rates at a torrent pace about 18 months ago and has seen significant progress in bringing down inflation. Meanwhile, the economy has remained relatively strong. The Federal Reserve expected to see more of an impact on the economy due to the tighter monetary policy. Recent projections indicate that inflation will not reach the Fed’s target until 2026. As a result of this combination, The Federal Reserve has stated they intend to leave interest rates higher for longer, has lowered projections of rate cuts in 2024, and continues to administer quantitative tightening by reducing their swollen balance sheet of treasuries.

2) Longer-term interest rates have risen significantly as of late for a multitude of reasons. First, there is a wave of new supply. Shortly after the debt ceiling raised, the US Treasury began issuing more bonds to pay for the countries growing debt. Second, the largest purchasers of our bonds have a reduced appetite as of late. Japan and China have not been wanting to buy as much. Finally, continued political dysfunction in Washington has caused rating agencies to put US debt on credit downgrade watch.

3) Equity and fixed income markets in the third quarter appear to finally be starting to believe the Federal Reserve and that higher rates and tighter monetary policy are here to stay and will be the new norm….at least new in the last 15 years. Investments have been repricing, assuming this new reality.

For more great insights, highlights, and financial education,

follow MDL Wealth Management on:

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk.

The economic forecasts set forth in this material may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.

3Department of the Treasury

4Bank of America Merrill Lynch

5Federal Reserve

6University of Michigan

7Bureau of Labor Statistics

8Institute for Supply Management

9Census Bureau